Dr Neelam Suri, gynaecologist at Indraprastha Apollo Hospital, New Delhi, has her hands full. Part of her job is not only to guide expectant mothers through their pregnancy and ensure a safe delivery but counsel them on out-of-pocket expenses and hefty hospital bills. “That’s because their health insurance policies do not cover all expenses and they’ve got to read between the lines,” she says.

If your insurance company agent is trying to convince you that the policy would cover 30 days pre-delivery and 60 days post-delivery costs, hospitalisation charges and delivery expenses, including pre and post-natal services, you would be mistaken. The reality is that the reimbursement may not be enough to take care of delivery, pregnancy-related complications or a medical condition that the newborn might have. Even policies that advertise themselves as providing a full maternity shield fall short of providing any meaningful coverage. That’s because they come with sub-limits — monetary caps on certain covers as a percentage of the total sum insured — that are not enough to take care of bills in big cities like Mumbai or Delhi.

Most insurance policies fall short of the very basics and cover just two births in a lifetime. They do not include consultation fee and diagnostic tests, provide for in-vitro fertilisation (IVF) procedures or cover the cost of supplements like vitamins and tonics either. Most importantly, they do not have anything for pregnant women over the age of 45.

KNOW YOUR WAITING PERIOD

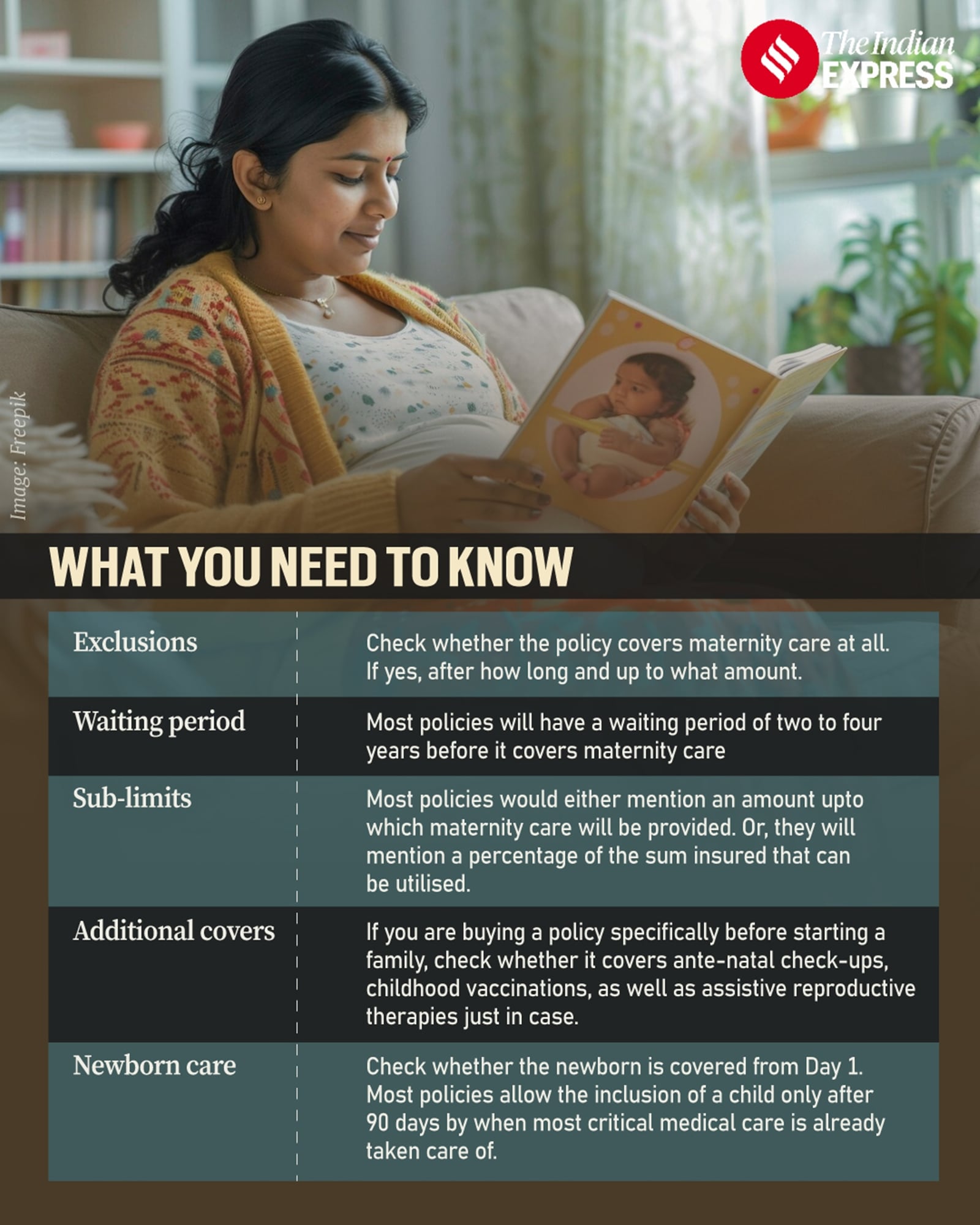

If you’re planning on starting or extending your family, buy your maternity insurance well in time. There is a 24-month waiting period for hospital admissions. Since babies can also come early, factor in premature births as well. “The waiting period can range from nine months to six years. The standard now, however, is about two years. Maternity benefits rarely come in-built and are given as add-ons,” says Tejas Jain, founder of BimaKavach, a platform that helps in choosing insurance policies. You cannot wait for pregnancy to secure your cover because policies consider it as a pre-existing condition and disqualify you from claiming benefits within the waiting period.

WHAT ARE EXCLUSIONS?

Most general health insurance policies exclude maternity care, except ectopic pregnancy, a high-risk condition when the fertilised egg attaches itself outside the uterus, most often the fallopian tube that carries the egg to the uterus. A policy by a big insurance provider covers the expenses of a delivery as well as the pre- and post-natal check-ups only up to limits mentioned, but “subject to a maximum of two deliveries in the entire lifetime of the insured person.”

Points to keep in mind while getting a maternity insurance scheme

Points to keep in mind while getting a maternity insurance scheme

The sub-limit is meagre. The policies pay up to Rs 20,000 for C-section deliveries for a Rs 5 lakh coverage, Rs 40,000 for a Rs 7.5 lakh coverage and a maximum of Rs 1 lakh on policies for Rs 50 lakh and above. The amount covered in the most commonly purchased policies of Rs 5 lakh and Rs 7.5 lakh is unlikely to cover expenses at nursing homes in big cities like Delhi and Mumbai. At bigger hospitals, even the sum of Rs 1 lakh may not be sufficient for mothers who need multidisciplinary care. “The cost of maternity care in cities like Delhi and Mumbai can range anywhere between Rs 30,000 and Rs 40,000 for an uncomplicated delivery in small hospitals and nursing homes. In bigger, tertiary care hospitals, the cost is likely to be upwards of Rs 1 lakh, more if the person opts for suites and additional services. The cost also goes up in cases where the mother might have other conditions for which a multi-disciplinary team of doctors is required,” says Dr Suri.

WHAT ABOUT IVF AND ADD-ONS?

Although infertility is a growing concern, existing insurance does not cover assisted reproductive technologies such as IVF and surrogacy. Harvesting and storing stem cells are not covered either. There is a provision for add-ons for a more comprehensive care but again, the limits offered are very little. One such add-on that covers all antenatal check ups, delivery, and even assisted reproductive technologies provides an annual maternity cover for Rs 5,000 a year for a Rs 5 lakh policy, Rs 12,000 for a Rs 10 lakh policy and Rs 25,000 for a Rs 50 lakh plus policy. Any sum that is not used gets added to the next year’s kitty. This is a good thing because for the cheapest variants, the policy has a waiting period of four years for maternity benefits. Some add-ons provide a Rs 10,000 support for tests conducted on a child at the time of adoption, yet others offer a discount of up to Rs 25,000 on maternity packages available at a select network of hospitals. While some websites advertise stem cell preservation, there’s no clause specifying it.

IS THERE A COVER FOR COMPLICATIONS?

Since policies do not cover maternity care, they do not cover complications arising from it, except ectopic pregnancies. “A complication leads to longer hospital stays and an increased expenditure by way of doctor fees and medicines — all of which are necessary clinically. Yet these are kept out of the purview of insurance,” says Dr Suri. In fact, she finds maternity policies offered by large corporate houses and PSU companies providing the most holistic coverage. These are likely to cover termination of pregnancy in cases where the foetus has certain genetic defects or the mother is at risk.

IS YOUR NEWBORN PROTECTED?

Most policies offer coverage to newborns only 90 days after birth. This means there is no protection during the crucial period when a newborn with health issues might need to be admitted to the neo-natal intensive care unit (NICU). Parents would need to pay nearly Rs 10,000 a day for a NICU bed in addition to medicines, consumables and doctors. A few policies include newborn benefits from Day 1. However, there are sub-limits up to 25 per cent of the sum insured. That means you get only about Rs 1.25 lakh for a Rs 5 lakh policy.

Clearly, there are gaps that need to be addressed and worked on, considering maternal and child health are foundational benchmarks of a nation’s public health status. “Maternity care was never covered by insurance policies until about a few years ago because maternity is not considered a disease. It was only when private companies entered the market that a need for maternity coverage was felt and such add-ons were introduced,” says Jain. However, with couples investing big amounts, we might see companies in a race to tempt them with special packages.

link