Dublin, July 02, 2024 (GLOBE NEWSWIRE) — The “Global Healthcare BPO Market by Outsourcing Models, Provider (Patient Care, RCM), Payer (Claims Management, Billing & Accounts), Life Science (R&D, Manufacturing, Sales & Marketing (Analytics, Research)), & Region (Source, Destination) – Forecast to 2029” report has been added to ResearchAndMarkets.com’s offering.

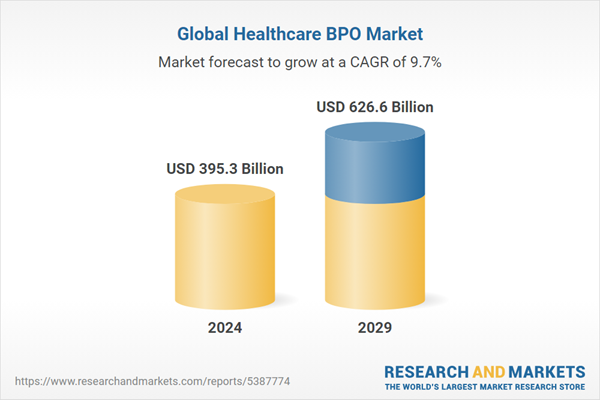

The global healthcare BPO market is projected to reach USD 626.6 billion by 2029 from USD 395.3 billion in 2024, at a CAGR of 9.7% from 2024 to 2029

The growth of the healthcare BPO market is being driven by increased pressure to reduce rising healthcare costs and the growing trend of outsourcing in the pharmaceutical and biopharmaceutical industries. Factors such as advanced data analytics and the increasing adoption of artificial intelligence-based tools for drug discovery are presenting lucrative opportunities for market expansion in the forecast period. However, limitations in the data capturing process in Medicaid services pose challenges to the market’s growth.

The integrated front-office services and back-office operations segment is estimated to account for the second-largest share in Healthcare BPO market.

Based on payer services, the segment is divided into claims management services, integrated front-end services and back-office operations, member management services, product development & business acquisition services (PDBA), provider management services, care management services, care management services, billing and accounts management services and HR services. Among these, integrated front-end services and back-office operations is estimated to account for the second-largest share in the healthcare BPO market. This is due to their pivotal role in optimizing operational efficiency for healthcare payers.

By outsourcing tasks like mailroom services, data scrubbing, and round-the-clock contact center support, payers can significantly reduce operational costs while enhancing service quality. This strategic outsourcing allows payers to focus on their core competencies, streamlining their operations and improving overall business performance.

Furthermore, the rising expectations of customers, including the demand for 24-hour service availability, are driving the need for outsourcing these functions. By entrusting these critical tasks to specialized BPO providers, payers can ensure prompt complaint and query resolutions, efficient customer relationship management, and seamless service delivery, thus solidifying the prominence of integrated front-end services and back-office operations in the healthcare BPO landscape.

Sales and marketing service segment accounts for the largest share in healthcare BPO market during the forecast period by non-clinical services.

Based on life science services segment, the healthcare BPO market is segmented into manufacturing, research and development, and non-clinical services. The non-clinical service segment is further divided into sales & marketing services, Supply chain management & logistics services, and other non-clinical services. Among these the sales and marketing services segment accounts for the largest share in healthcare BPO market. The dominance of sales and marketing services in the non-clinical services segment of the healthcare BPO market is primarily attributed to the intricate regulatory landscape within the pharmaceutical industry.

With regulations constantly evolving, pharmaceutical companies are compelled to allocate their resources towards core activities such as research and development, and production. Consequently, this has intensified the demand for specialized marketing services to navigate the complex regulatory environment effectively.

Moreover, the necessity for extensive field forces has spurred the emergence of contract sales organizations in the pharmaceutical sector. These organizations offer tailored sales solutions, augmenting the marketing efforts of pharmaceutical companies while allowing them to focus on their core competencies. As a result, the sales and marketing segment has garnered the largest share in the non-clinical services segment of the healthcare BPO market, reflecting the indispensable role it plays in facilitating pharmaceutical companies’ compliance with regulations and enhancing their market presence.

US holds the second largest segment in healthcare BPO market by destination geography during the forecast period.

In this report, the healthcare BPO market is segmented into source geography and destination geography. The source geography is divided into North America, Europe, and rest of the world, but the destination geography is further divided into India, US, Bulgaria and other EU countries, Philippines, China, Brazil, Kingdom of Saudi Arabia, and rest of the world.

Among the destination geography segment, US holds the second largest position in the healthcare BPO market. This is due to a surge in the adoption of computer-assisted Revenue Cycle Management (RCM) coding systems. This uptick in RCM adoption among healthcare providers is primarily driven by the imperative to enhance operational efficiency, reduce costs, and minimize errors.

As healthcare organizations increasingly recognize the benefits of leveraging advanced technology for streamlining their revenue cycles, the demand for outsourcing services in the US has correspondingly expanded. Outsourcing providers located in the US are strategically positioned to cater to this growing demand, offering specialized expertise in RCM optimization and leveraging their proximity to clients to provide tailored solutions.

Additionally, the intricate and evolving regulatory landscape in the US healthcare sector necessitates a nuanced understanding of compliance requirements, further bolstering the demand for outsourcing services from domestic providers. Thus, the combination of technological advancements, cost-effectiveness, and regulatory complexities propels the United States to maintain its substantial presence as the second-largest destination for healthcare BPO services.

Key Attributes:

| Report Attribute | Details |

| No. of Pages | 369 |

| Forecast Period | 2024 – 2029 |

| Estimated Market Value (USD) in 2024 | $395.3 Billion |

| Forecasted Market Value (USD) by 2029 | $626.6 Billion |

| Compound Annual Growth Rate | 9.7% |

| Regions Covered | Global |

Premium Insights

- Growing Need to Reduce Healthcare Costs to Drive Market Growth

- Revenue Cycle Management Segment Accounted for Largest Share in North America

- Manufacturing Service to Dominate Market During Forecast Period

- Sales & Marketing Service Segment to Dominate Non-Clinical Service Market

- Analytics Service Segment to Account for Largest Share in Sales & Marketing Service Market

- India to Register Highest Growth During Forecast Period

Market Dynamics

Drivers

- Shift to Icd-10 Coding Standards and Upcoming Icd-11 Standard

- Pressure to Reduce Rising Healthcare Costs

- Loss of Revenue due to Billing Errors

- Demand for Niche Services

- Need for Structured Processes and Documentation

- Lack of In-House Expertise in End-use Segments

- Growing Outsourcing in Pharma and Biopharma Industries

Restraints

- Hidden Outsourcing Costs

- Concerns Related to Losing Visibility and Control Over Business Process

Opportunities

- Advanced Data Analytics

- Growing Adoption of Artificial Intelligence-based Tools for Drug Discovery

Challenges

- Limitations in Data Capturing Process in Medicaid Services

- Data Security Concerns

Outsourcing Approaches

- Bundled Services

- Fee for Service

- Flexible Contracts

- Best-Shore

Outsourcing Models

- Multi-Sourcing

- Captive Center

- Hybrid Delivery Model

- Preferred Provider

- Strategic Partnership

- Global Delivery Model

Industry Trends

- Digital Transformation

- Rise in Telehealth and Remote Services

- Focus on Revenue Cycle Management (Rcm)

Key Technologies

- Artificial Intelligence and Machine Learning

- Robotic Process Automation

- Cloud Computing

Complementary Technologies

- Wearable Devices and Remote Monitoring Tools

- Augmented Reality and Virtual Reality

- Data Analytics and Business Intelligence

Adjacent Technologies

- Natural Language Processing (Nlp)

- Internet of Medical Things

- Blockchain

Company Profiles

Key Players

- Accenture PLC

- Cognizant Technology Solutions Corporation

- Tata Consulting Services Limited

- Xerox Corporation

- Wns (Holdings) Limited

- Ntt Data

- Iqvia Holdings Inc.

- Mphasis

- Genpact Limited

- Wipro Limited

- Infosys Bpm

- Firstsource

- International Business Machines Corporation

- Gebbs Healthcare Solutions

- Capgemini SE

Other Players

- Omega Healthcare Management Services

- R1 Rcm

- Invensis Technologies

- Unitedhealth Group

- Hcl Technologies Limited

- Parexel International

- Access Healthcare

- Sutherland Global

- Akurate Management Solutions

- Ags Health

For more information about this report visit

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

- Global Healthcare BPO Market

link